The EU CBAM poses an immediate and serious operational threat for organisations that import goods covered under this regime into the EU. Redshaw Advisors is committed to enhancing strategic decision-making ability by creating up-to-date transparency on the CBAM legislation, direct and indirect cost forecasting, MRV (Messure Report and Verify) requirements and risk management recommendations for organisations exposed to the EU CBAM

EU Carbon Border Adjustment Mechanism (CBAM): A Guide for Importers and Businesses

The EU CBAM, a crucial component of the Fit For 55 packages, to combat carbon leakage. The CBAM achieves this by adjusting the embedded cost of direct and indirect emissions from importers into the EU. Initially, the package focuses on sectors such as iron and steel, aluminium, cement, fertiliser, electricity, hydrogen, chemical precursors, and specific downstream articles. Additional sectors like paper, plastics, organic chemicals/polymers, glass, and oil refining are likely to be added after the 2025 transitional period. The CBAM will cover around 750 individual products defined within customs commodity codes, eventually encompassing all products covered by the ETS without any materiality threshold.

Dan Maleski

Environmental Markets Advisor

Connect with me

Who will be impacted by the EU CBAM?

As a result of the EU CBAM’s scope into downstream articles, including items such as such as screws, nuts, bolts and similar products of iron or steel. A significant amount of importers will have a newly incurred compliance obligation as a result of this legislation.

A few of the many industries impacted are:

- Construction companies and material distributors (cement, aluminum, iron, steel)

- Automotive and aerospace manufacturers (aluminum, iron, steel)

- Advanced manufacturing (aluminum, steel)

- Chemicals companies (precursors, fertilizers)

- Food retail value chain (aluminum foil)

Questions to consider:

- How do I know if my company is subject to CBAM

- How much will my exposure to the EU ETS change as a result of CBAM

- What is the penalty if I don’t comply

- Will I need a new registry account

- How will I measure and report my emissions

- What will the financial impact be as a result of this regulation

- What is a punitive default value

- What is a system boundary

- Is verification required during the transition period

How Certificates will work

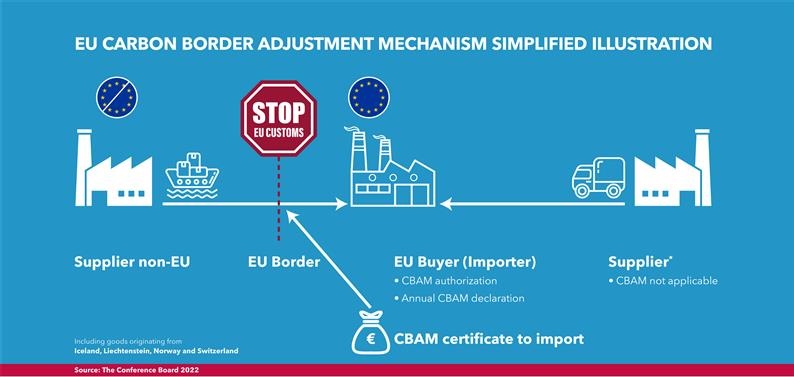

Importers in the EU will be required to purchase CBAM certificates. The certificate price will be calculated based on the average weekly auctions of the EU ETS. If no auctions are held in a given week, the price will be set up as the average of the previous week.

The CBAM certificates cannot be traded, have limited validity (July 1st of each year, commencing 2027), and can only be sold to authorised declarants.

The surrender deadline for CBAM certificates is May 31st of each year, starting in 2027.

The transaction platform for CBAM certificates will be the CBAM Registry, managed by the European Commission.

The authorised CBAM declarants shall ensure that the number of CBAM certificates on their CBAM registry account at the end of each quarter matches at least 80% of their embedded cost of carbon in imported products.

The threshold of 80% of imported goods (required each quarter) which is based on default values.

In cases where imported products have already been subject to robust carbon pricing in their country of origin, the paid carbon price can be reduced from the EU CBAM charges, provided evidence is available. For products where reasonable benchmark values cannot be determined, default values will be published based on the emissions of the highest-emitting EU installations in that sector. However, using these default emissions values may result in higher prices than actual emissions. Importers can demonstrate actual emissions during a reconciliation procedure and surrender the appropriate number of CBAM certificates accordingly.

In case CBAM declarants want to sell back an excess of CBAM certificates back to the member states, submission is required by July 30th each year (starting 2027). Please note, the maximum amount of CBAM certificates an authorised declarant can sell back is 1/3 of the total number of certificates purchased for one year. The repurchase price of CBAM certificates will match the same price as the certificates were originally bought.

The Transitional Period Oct 2023 – Dec 2025

The transitional period for the CBAM begins on October 1st, 2023, and extends until 2026. During this period, importers within the scope of the CBAM must report emissions embedded in their goods at the time of import into the customs territory of the EU. Once the transition period concludes, the CBAM’s scope will be re-evaluated to determine if additional products and services, including indirect emissions, should be included. Another important clarification to be addressed is the methodology used to determine the carbon intensity of imported goods. The revaluation of sectors exposed to the CBAM will take place one year before the end of the transitional period.

Likely sectors to be added in after the 2025 transitional period:

- Paper & Pulp

- Plastics

- Organic Chemicals and or polymers

- Glass

- Oil Refining

Solutions

Understanding the EU CBAM and its implications is crucial for businesses both within Europe and abroad. At Redshaw Advisors, we are dedicated to empowering strategic decision-making by providing up-to-date transparency on the CBAM legislation. We offer valuable insights into direct and indirect cost forecasting, MRV requirements, and risk management recommendations for companies already exposed to the EU ETS, as well as importers required to participate in this regime.

Schedule a call with our CBAM advisors to address the following key questions:

- How do I determine if my company is subject to CBAM?

- What changes can I expect in my exposure to the EU ETS due to CBAM?

- What are the penalties for non-compliance?

- Will I need a new registry account?

- How do I measure and report my emissions?

- What will be the financial impact of this regulation?

More About CBAM

Steel sector concerns remain post CBAM implementation

The steel sector’s concerns regarding the implementation of the transitional phase of the European Union’s Carbon Border Adjustment Mechanism (CBAM) remain…

Reporting Recommendations and Requirements for the EU CBAM

The CBAM’s reporting requirements, introduced through the Implementing Regulation, constitute one of the most extensive sets of greenhouse gas (GHG) emissions reporting requirements…

Measurement of embedded emissions and compliance with EU CBAM

The Implementing Regulation outlines the procedures for monitoring and calculating the embedded emissions of imported products. The specific rules for calculating these emissions…