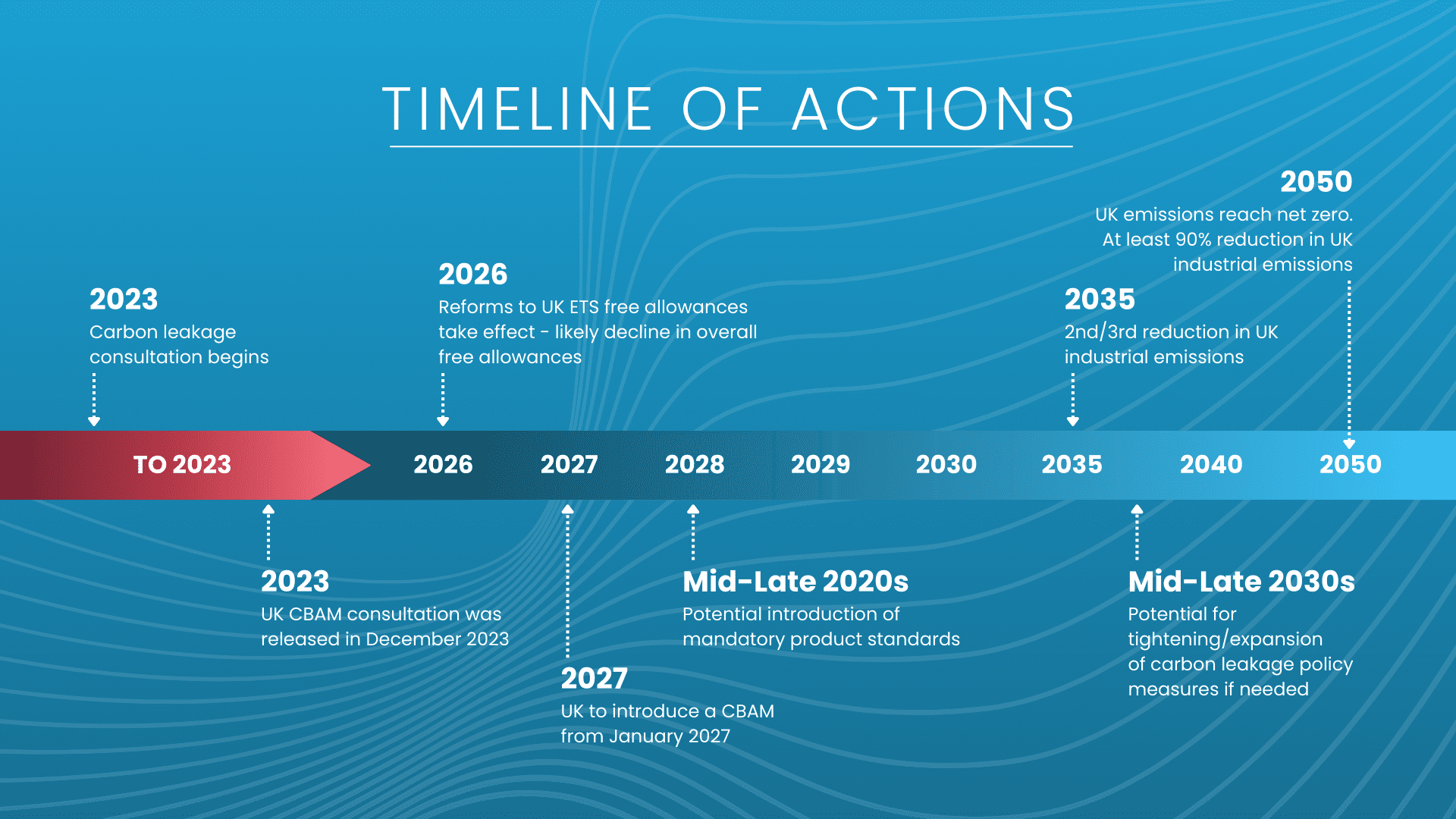

Carbon leakage refers to a situation where businesses or industries move their production (and associated carbon emissions) to regions with less stringent carbon regulations to avoid the higher costs of compliance. This can undermine the effectiveness of emissions reduction measures in one region while increasing emissions in another.

Contact Redshaw Advisors today for valuable insights and strategic decision-making aid on CBAM implications.

Contact Us Today by calling +44 20 3637 1055 or email us by completing the form below.