Market developments:

- Carbon falls ~2% despite intra-week surge

- Prices hit €9.48 mid-week but fail to top previous high

- Cold weather and compliance buying providing support

- Clean Dark Spreads recover some of 2018’s losses

- UK should align green energy policies with EU

- Renewable generation continues to grow

- The Daily Market update is back for those looking to purchase allowances for year-end compliance requirements. To receive it please click here.

EU Allowance Auction Overview:

- Auction volume up at ~21.5 Mt this week, the largest weekly volume in 2018 to date

- Return of UK auctions brings February auction total up to ~84.2Mt

- See auction timetable below

EUA PRICE ACTION

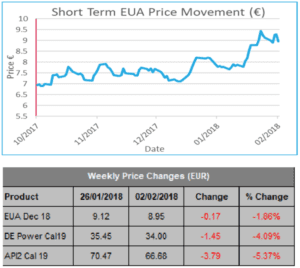

The week began with a continuation of the previous week’s decline as carbon drifted lower. Support was found around €8.80 and a strong auction on Wednesday helped propel prices higher. With no obvious trigger for the gains it is likely some short covering and more reliable cold weather forecasts were the main drivers. Prices tried, and ultimately failed, to move both higher and lower throughout Thursday and ended in the middle of the day’s range, suggesting a balanced supply and demand picture. The trading week ended on Friday with the bears on top when most of Wednesday’s rally was reversed and EUA prices tumbled 34c to close at €8.95. The fundamental picture actually improved as the week progressed thanks to cold weather, improving clean dark spreads and an intra-week surge in gas prices. Price Impact: carbon has drifted off from highs rather than plummeted back to pre-Christmas levels telling us that the demand side of the market is still too strong to allow the market to experience a major correction.

The week began with a continuation of the previous week’s decline as carbon drifted lower. Support was found around €8.80 and a strong auction on Wednesday helped propel prices higher. With no obvious trigger for the gains it is likely some short covering and more reliable cold weather forecasts were the main drivers. Prices tried, and ultimately failed, to move both higher and lower throughout Thursday and ended in the middle of the day’s range, suggesting a balanced supply and demand picture. The trading week ended on Friday with the bears on top when most of Wednesday’s rally was reversed and EUA prices tumbled 34c to close at €8.95. The fundamental picture actually improved as the week progressed thanks to cold weather, improving clean dark spreads and an intra-week surge in gas prices. Price Impact: carbon has drifted off from highs rather than plummeted back to pre-Christmas levels telling us that the demand side of the market is still too strong to allow the market to experience a major correction.

WEEK AHEAD

We expect compliance buying to play a more prominent role through February as once-a-year buyers armed with their verification reports come to market. This will provide support for carbon, as will the cold weather that is currently gripping most of Europe. The return of the UK auction on Wednesday means the market will be supplied with more than 21.5Mt, the highest weekly volume so far in 2018, but no higher than the market ably coped with last year. Aside from these minor influences there is little change in the overall bearish fundamental picture, the generation spreads are still far lower than the end of 2017 and are at levels unlikely to persuade utilities to materially advance hedging, so we favour prices continuing to drift off.

That said, over the last 6 months we have seen prices retreat from ‘surprising’ highs only to surge higher once more. With the timing of the speculative interest, that is trying to get ahead of the start of the MSR, impossible to calculate, such price action could well be a recurring theme through 2018.

OTHER NEWS

UK should align green energy policies with EU after Brexit.

The UK should seek to remain closely aligned with the EU on energy and climate change after Brexit next year, said industry association Energy UK. According to Energy UK the UK’s future relationship with the EU should contain an “energy and climate chapter” to ensure stability and continued progress in achieving climate change at minimal cost to energy consumers.

The association added that leaving the EU Emissions Trading Scheme (ETS) without a replacement carbon trading structure in place could jeopardise the UK’s prospects of meeting its long-term emissions reduction targets. The UK government should at the very minimum ensure that the country remains a part of the EU ETS until the end of 2020. Allowing the UK to remain a part of the ETS would also be of benefit to the EU’s goals of meeting its own targets.

Renewable generation continues to grow.

For the first time, the European Union generated more electricity from wind, solar and biomass than from coal in 2017, according to new analysis. Five years ago, coal generation was more than twice that of wind, solar and biomass.

Despite this new milestone, EU power sector emissions were unchanged in 2017. Low-carbon sources met 56% of demand, a figure that is unchanged since 2014. Wind, solar and biomass now supply more than a fifth of the electricity generated in the EU, at 20.9%, up from less than 10% in 2010, with coal at 20.6%, however nuclear remains the single-largest source of electricity, generating 25.6% of the EU’s power.