All information is accurate as of 13th February 2026

Author: Sawal Bacha

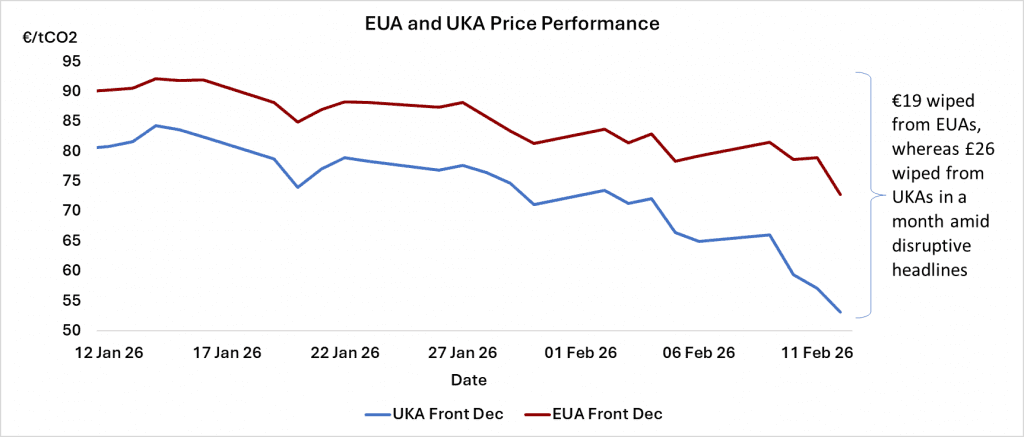

Following a bullish start to 2026, with EUA prices reaching a 31-month high at €93.80 and UKA prices climbing to a 33-month high at £75.45, both carbon markets have tumbled as a series of political and geopolitical headlines collided to precipitate an investor sell off.

Source: ICE. Redshaw Advisors

EUA prices have come under pressure in the last week as several headlines have emerged, with politicians and market commentators across the EU raising the prospect of EU ETS amendments and casting doubt on the fundamental balances in the coming years. Those fundamental balances have created a bullish narrative and led investors to build record length with the prospect of higher prices due to a supply shortfall.

The UK market has also had its own troubles with prices plunging amid rumours of setbacks in linking negotiations and speculation over the future of UK Prime Minister Keir Starmer. With much of the recent upside in the UK market coming due to the prospect of linking, the political turmoil has increased the risk around linking and led to a rethink among investors.

However the scale of the declines in recent days have far exceeded anything seen in the previous few weeks as the investor length begins to unravel at a faster pace as losses mount.

UKAs plunged £7.50 in an hour on Wednesday and at one point stood more than 17% down on the day, setting an 10-month low at £42.88. But yesterday it was the turn of the EU market to lead the charge lower. The already nervous markets were spooked again as traders reacted to remarks from Germany’s Chancellor Merz in which he suggested if the EU ETS isn’t working for Europe, it should be revised or postponed. The comments were the latest in a long line that included Czech, Belgian and Italian leaders, who argued that current EUA prices were too high and harmful for EU industry. In addition, earlier remarks by ex‑DG CLIMA head, Jos Delbeke, suggested releasing unallocated allowances to the market ahead of the current 2031-2032 timeline, while German MEP Peter Liese, a leading figure in the 2022 EU ETS reforms, suggested delaying the phase-out of free allowances.

As a result, investors took another step back and the long squeeze drove EUAs to a €72 (a 6-month low), marking their steepest single-day drop since November 2022.

Where both markets go from here is difficult to predict, the only certainty is more volatility. There remains considerable length in both markets, so there is certainly potential for more washout and the downside that will come with it. However, analysts appear united in their expectations for any amendments to come via the ETS review pencilled for Q3 this year and the potential timeline for any intervention looks to be 2028 at the earliest, leaving the 2026 and 2027 fundamental bull story intact.

For the UK market, near term price expectations hinge on linking. The discount to EUAs has blown out to more than £19 in recent days but one positive linking headline could send UKAs surging higher once more.

To access the full analysis and stay ahead of market movements, get in touch about our monthly reports. Each edition delivers clear performance analysis, forward-looking price outlooks, and expert interpretation of the policy, macro, and trading signals shaping carbon markets, giving you the confidence to understand what's happening and decide what to do next.

Contact us on +44 20 3637 1055 or email us here.