All information is accurate as of 6th March 2026

Author: Tom Lord

After a strong sell off in February, the war in the Middle East looks set to drive price action in March with contrasting impacts for the UK and EU carbon markets.

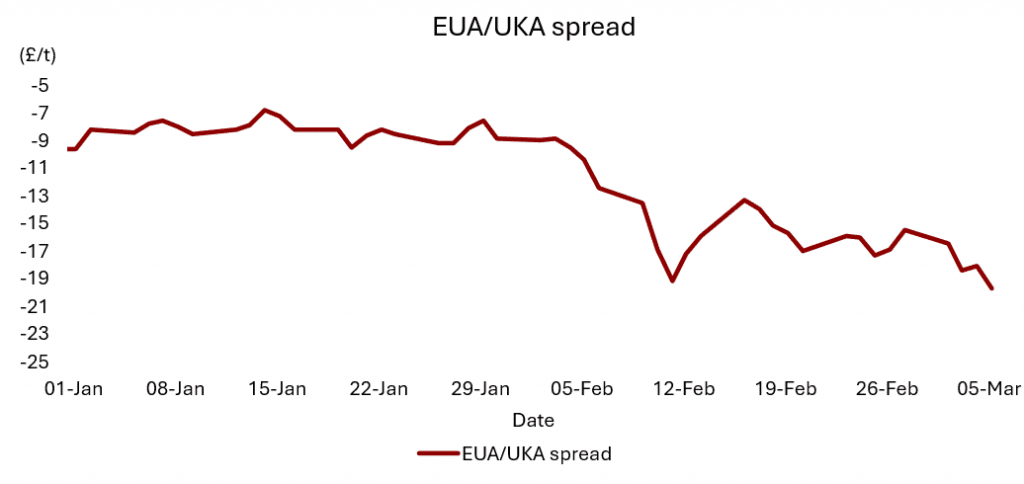

Both carbon markets ended February significantly lower as a series of ETS reform calls dented investors’ confidence in the bullish EUA outlook, weighing on prices with more than 37Mt of net Investment Fund length unwound. It was a similar story in the UK market, where some negative headlines around linking with the EU ETS, coupled with the political turmoil surrounding PM Starmer’s ability to retain control weighed on UKAs. The EUA sell off added to the bearish sentiment in the UK market and saw the UKA discount to EUAs blow out to more than £19.

Source: ICE, Redshaw Advisors

The start of the Middle East conflict on the last day of February ensured the markets started March in a volatile fashion. European and UK gas prices more than doubled in two days at their peak amid disruptions to the Strait of Hormuz, a crucial point of transit just off the coast of Iran for 25% of global oil supplies and 20% of the world’s LNG shipments. Iran has already warned vessels they will be attacked if they attempt to pass, and Trump’s promise to insure and protect ships transiting has not eased the current shipping standstill in the region.

For the carbon markets, the impact of the war will largely depend on its duration and the ability of energy shipments to move through the Strait of Hormuz. Higher gas prices resulting from the reduced LNG supply create a bullish impact for EUAs as the gas-to-coal fuel switch in power generation raises emissions. However, a protracted conflict will also increasingly lead to industrial demand destruction due to the high energy prices. This will not only reduce industrial EUA hedging requirements but also power sector emissions as power demand from the industrial sectors falls away.

For UKAs, the conflict is a more bearish development. The UK has already phased out all the coal fired power generation, leaving it no option but to continue burning higher priced gas. Not only will this lead to industrial demand destruction, but cheaper EU power will also incentivise maximum power imports from the EU, further reducing UK power generation and the hedging needs of the UK power sector.

For both the UK and EU, the conflict will hamper their already fragile economic recoveries. Inflation may also once again become a problem as interest rate rises to try and counteract inflation cannot be ruled out.

So far, EUAs have been relatively stable while UKAs have continued to slump. From here, the only certainty would appear to be volatility as the markets react to developments in the Middle East.

To discuss the outlook in more detail or understand how Redshaw Advisors help companies understand and manage their exposure to carbon markets, please get in touch.