Market developments:

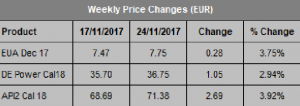

- Carbon gains 28c to end the week at €7.75

- The failure to break lower or scale new highs leaves carbon in ‘no man’s land’

- Clean dark spreads suffer as coal prices rise substantially, tempered slightly by a strong Euro

- Member States back the Phase IV reforms as worries over UK vote prove to be unfounded

- Worried about EU ETS Brexit risk? Contact us to join our confidential EU ETSinstallations-only working group

EU Allowance Auction Overview:

- Auction volume down slightly to ~22.6Mt this week, from 23.2Mt last week

- December auction volumes fall to ~53.5Mt

- See auction timetable below

EUA PRICE ACTION

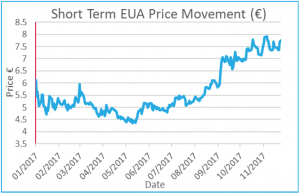

Carbon advanced nearly 4% to close the week at €7.75 despite last week’s price influences all pointing to further downside. However, few clues were provided to the direction carbon will take next as price failed to break out in either direction. Once again, the week began with falls in price, as expected, as carbon traded down to €7.20, but similar to last week support was found and carbon managed to recover the lost ground the same day. Prices then traded in a relatively tight range for a few days, despite a brief surge higher due to Member States approving the Phase IV reform file (see Other News). Thursday saw the main price action of the

Carbon advanced nearly 4% to close the week at €7.75 despite last week’s price influences all pointing to further downside. However, few clues were provided to the direction carbon will take next as price failed to break out in either direction. Once again, the week began with falls in price, as expected, as carbon traded down to €7.20, but similar to last week support was found and carbon managed to recover the lost ground the same day. Prices then traded in a relatively tight range for a few days, despite a brief surge higher due to Member States approving the Phase IV reform file (see Other News). Thursday saw the main price action of the  week as prices surprised to the upside moving 28c higher as a result of a strong auction seemingly caused by cold weather forecasts. However, Friday saw no follow-through and the bull run ran out of steam well short of November’s high of €8.02. The failure to break lower at the start of the week and scale new highs at the end leaves carbon in no-man’s land. Elsewhere, the clean dark spreads fell, in theory reducing the demand for carbon. However, rising gas prices and nuclear availability issues are likely to cancel out the bearish influences for now. Price Impact: there were several bearish influences present last week and prices tried, but ultimately failed, to go lower. That carbon could not go lower suggests demand either from utility hedging and/or new speculative interest in the market continues to leave the market short.

week as prices surprised to the upside moving 28c higher as a result of a strong auction seemingly caused by cold weather forecasts. However, Friday saw no follow-through and the bull run ran out of steam well short of November’s high of €8.02. The failure to break lower at the start of the week and scale new highs at the end leaves carbon in no-man’s land. Elsewhere, the clean dark spreads fell, in theory reducing the demand for carbon. However, rising gas prices and nuclear availability issues are likely to cancel out the bearish influences for now. Price Impact: there were several bearish influences present last week and prices tried, but ultimately failed, to go lower. That carbon could not go lower suggests demand either from utility hedging and/or new speculative interest in the market continues to leave the market short.

WEEK AHEAD

The continued support for carbon combined with cold weather forecasts, uncertain nuclear availability and an auction shutdown on the horizon makes lower prices into the end of 2017 look less likely as each week passes. The market may be susceptible to price rises during the auction shutdown, as witnessed last year, and compounded by the uncertainties surrounding French nuclear availability. What we don’t know is what the weather holds in store and whether or not utilities and speculators have learned from last year’s auction shut down related price volatility and gone long in anticipation of a windfall gain. Volatility looks to be the most certain outcome. With just 3 weeks of full auction volumes left in 2017 and robust short-term demand signals, an early industrial Christmas present of prices below €7 seems unlikely. The Brexit clause is scheduled to be discussed in the Climate Change Committee meeting on 30th November and will likely provide some volatility this week. In the absence of stronger price rises last week and nothing too interesting this week we have a neutral outlook for the week with a watchful eye on temperatures and the Brexit clause developments.

OTHER NEWS

Member States back Phase IV reforms as UK votes to approve

Member States backed the Phase IV (2021-2030) reform package last week with just Croatia voting against the reforms. Going into the vote there had been fears the UK would vote against the reforms in protest at the Brexit clause that will render UK issued allowances from 1st January 2018 invalid. The fears proved unfounded as the UK backed the reforms.

The reforms now go to the ENVI Committee for a vote that is scheduled to take place on 28th November, however, the final approval from the plenary is not expected to take place until February 2018.

EU-Swiss ETS link up could begin on 1st January 2019

The link between the EU ETS and the Swiss ETS is expected to be in place at the beginning of 2019. After years of delayed negotiations politicians are finally making headway with the European Parliament expected to give formal approval in early 2018. The Swiss ETS is small in comparison to the EU ETS and the link up is expected to have no discernible impact on prices. However, a successful link up with the EU ETS will renew calls for other global links to be found.

European Commission brings Brexit proposal in line with German view

Amendments to the tabled Brexit proposal have brought the European Commission’s view much more into line with the German proposal according to reports by Argus Media. The proposal now specifically mentions Article 50 ensuring it only covers the UKs withdrawal from Europe. The proposal now also makes it clear that where a Member State with obligations lapsing uses national law to ensure compliance before the planned withdrawal date the measure must be repealed. Under the current proposal the Commission would still be able to invalidate UK issued allowances from 2019, making it uncertain whether the current proposal is sufficient for UK politicians.

The climate change committee in which all Member States are represented will discuss the proposal in a meeting on 30th November.

Redshaw Advisors have created a BREXIT IMPACTS discussion group that all EU ETS installations should join. We will provide regular Brexit updates as well as engage in Q&A discussion of the specific concerns of installations covered by the EU ETS. To encourage debate, participation in the discussion group will be anonymous and is reserved for EU ETS installations only. Join the group here.

Redshaw Advisors have produced a brief guide to the potential impacts of Amendment 47 here.

Final Phase IV compromise text gives further insight on the shape of Phase IV rules

The final compromise text on the Phase IV reforms provides further insight into the rules that will guide free allocation in Phase IV. We have picked out some of the more significant points for installations;

- Free allocation will drop to zero by 2030 for those not deemed to be exposed to carbon leakage

- Opt-out threshold kept at 25,000t

- Production increases or decreases of 15% will lead to free allocation amendments

- No more than 25% of auction revenues may be directed to indirect cost compensation

Please get in touch with the Redshaw Advisors team on +44 203 637 1055 for a more detailed analysis of the impact on your company.

COP23 moves the Paris Accords slowly forwards but little of note for EU ETS participants

The latest Conference of the Parties (COP) taking place in Bonn, Germany has advanced some technical points, including a review of progress towards achieving each countries Nationally Determined Contributions (NDCs) but has so far yielded little of relevance to EU ETS participants. COPs tend to look at national level issues such as the use of markets and targets as well as adaptation issues. The EU ETS plays an important role in NDCs of European countries, however, the rules and regulations of the EU ETS were not discussed in Bonn.